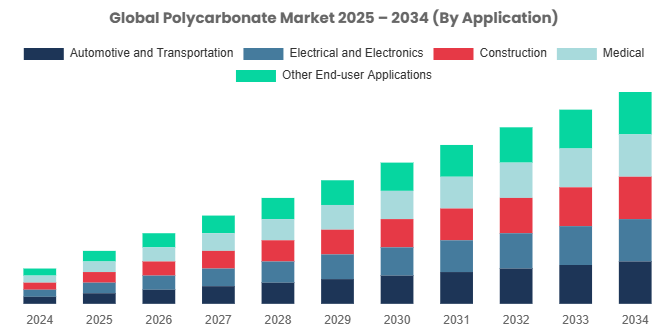

The Global Polycarbonate Market was valued at USD 24,999.69 million in 2025 and is anticipated to grow to USD 33,865.18 million by 2034, with a CAGR of 3.43% over the forecast period 2025 – 2034.

Polycarbonate Market Overview

Polycarbonate (PC) is a thermoplastic polymer that has wide applications due to its high impact strength, optical quality, and good thermal stability. All these make it applicable in a variety of uses in various industries such as in vehicles, electronics, construction, and medical devices.

The market for polycarbonate is growing rapidly worldwide. This is due to its vast applications in various industries such as in vehicles, electronics, and medical devices.

key driver

The most important driver for the market development is the rising need for light, strong, and shock-resistant materials in applications in the end-use. Polycarbonate possesses great chemical and physical properties, including its ability to be thermoformed, having a high degree of resistance to chemicals, and moisture resistance.

It is therefore ideal for use in several applications. Moreover, it is resistant to impact and highly transparent, making it ideal for use in vehicle parts, protective equipment, and building materials.

Price fluctuations of crude oil have a significant effect on the cost of producing Global Polycarbonate Market. Polycarbonate is a derivative of crude and heavy oil, and tough environmental regulations to curb plastic waste hinder the growth of the market.

For instance, the United Nations Environment Program (UNEP) has discovered that over 99% of polymers are made from crude oil and natural gas-based chemicals, which are poisonous and environmentally degrading sources. Hence, most nations are imposing rigorous laws to restrict the use of plastic, which could hamper market growth.

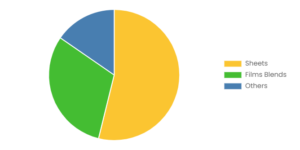

Increased need for Global Polycarbonate Market sheets across different industries offers great growth prospects. The panels are light, yet very strong and resistant to breakage and cracking when compared to glass. They have better features such as resistance to temperature, flexibility, durability, and installation ease.

This makes them suitable for uses like window glass, skylights, riot control devices, hospital devices, and food processing displays. The growing demand for polycarbonate sheets in these uses will propel the market growth.

The electronics segment leads the polycarbonate market with the highest share in 2024 and is likely to continue leading throughout the forecast period due to the light weight and high strength of polycarbonate in the market.

The rising demand for lightweight and high-strength materials in electrical products is anticipated to fuel the polycarbonate resin demand.

The Asia Pacific was the largest region in the polycarbonate sheet market in 2024 and is anticipated to be the most rapidly growing region in the forecast period. This is attributed to the presence of raw materials and cheap labor, making it the preferred location for manufacturers across various industries.

These producers continue to establish manufacturing facilities in the Asia-Pacific region in order to obtain higher profits. The worth of the polycarbonate market within the construction industry in China will increase in the forecast period. The central bank of the country can provide liquidity by adopting a non-aggressive monetary policy through favoring investment in new home starts.

The Italian construction sector is anticipated to expand as a result of government policy towards foreign direct investment (FDI) in manufacturing and government efforts to invest in energy, residential, and commercial projects to raise the demand for polycarbonate in the forecast period.

List of the prominent players in the Polycarbonate Market:

- Mitsubishi Engineering Plastics Corporation

- SABIC

- Covestro AG

- Ningbo Zhetie Daphoon Chemical Co. Ltd

- Chi Mei Corporation

- LOTTE Chemical Corporation

- EXOLON Group GmbH

- Trinseo SA

- Formosa Chemicals & Fibre Corp.

- LG Chem

- Teijin Limited

- Samyang Corporation

- Idemitsu Kosan Corporation Limited

- Centroplast Engineering Plastics GmbH

- Bayer Material Science AG

- Royal DSM

- Asahi Kasei Chemical Corporation

- Others